[ad_1]

There is no doubt that you have seen a variation of this chart Float around the Internet. It shows the 5 (or 10) largest companies in the Standard & Poor’s 500 Index, with an explanation of how much they have risen in the past few quarters (20-25%).

What about the remaining 490 companies? They are hardly optimistic and may rise by as much as 5%. Here is a longer qualitative argument (coming soon). Now, let’s focus on the quantity aspect.

This is not atypical behavior.We know from Academic Research Only a small number of stocks tend to drive the market up: only one of the 25 companies is responsible All stock market returns. The other 24 of the 25 stocks—96%—are basically worthless.Hendrick Besenbinder Observed: “About 30 stocks accounted for 30% of the net wealth generated by stocks since 1926, and 50 stocks accounted for 40% of the net wealth.”

This has not stopped the criticism that “only a few companies” are pushing the market. We have heard these complaints for about 5 years, but they haven’t really resonated much with traders and investors.

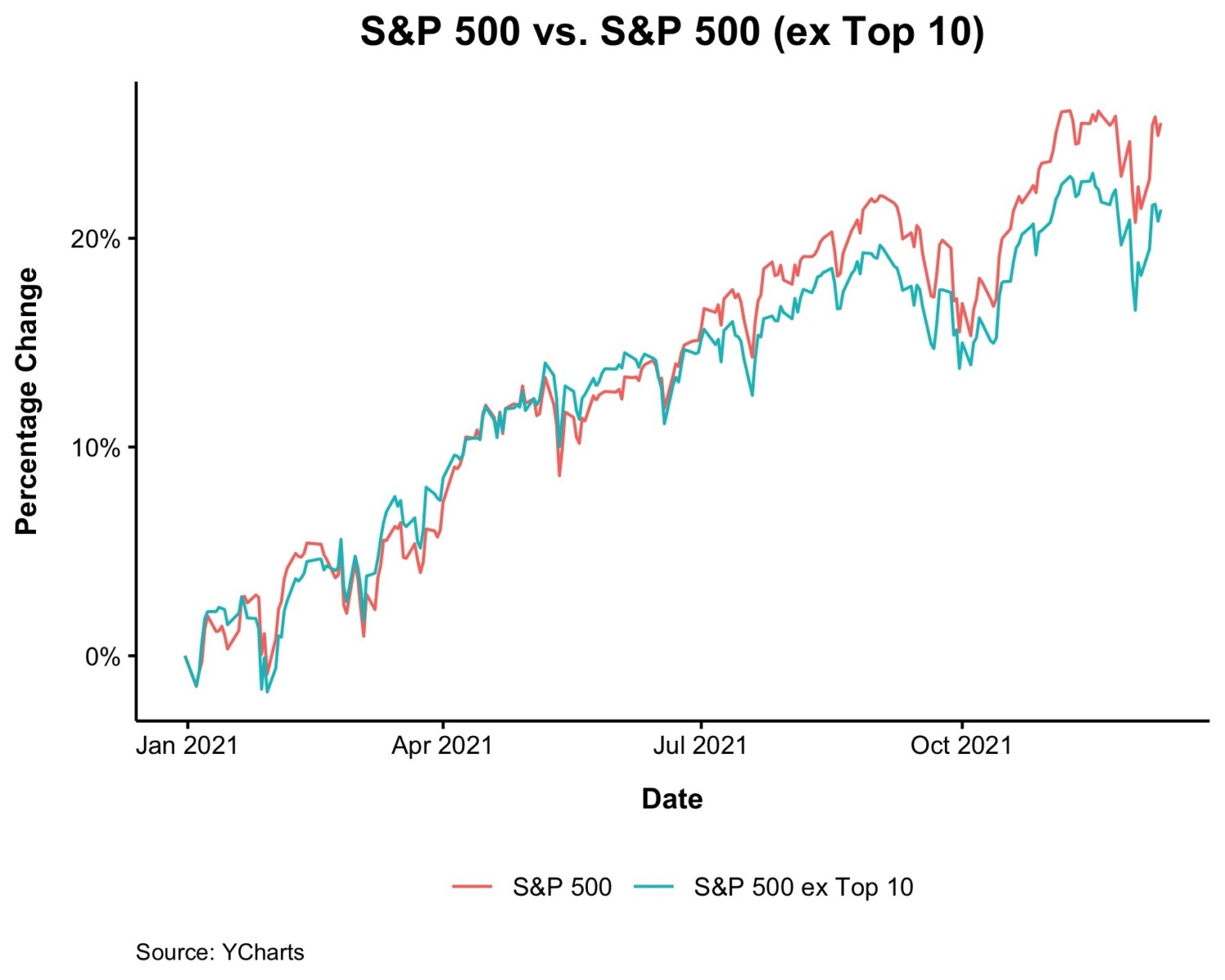

Consider, instead of just looking at the top 5 stocks and the remaining 495 SPX names, what would happen if you looked at the balances of 10, 25, 50, or 100 stocks and SPX? gap Made some charts for me.

It turns out that it hardly changes the chart:

The top 10 looks a lot like the top 5, but it shouldn’t be surprising-they are all large technology stocks, holding a highly concentrated share:

top 10

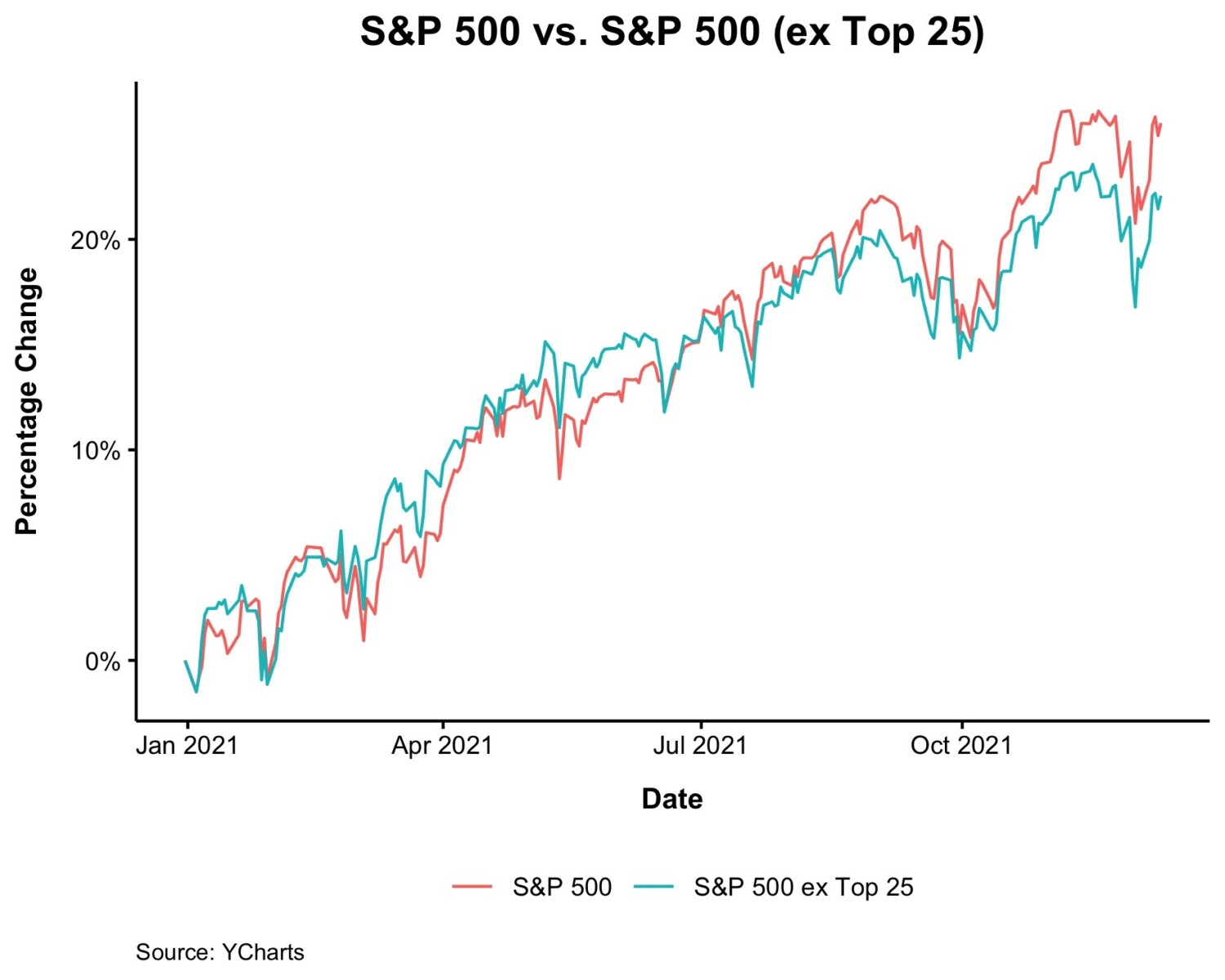

The top 25 still looks a lot like the top 5, with slightly worse performance, but not so much.

Top 25

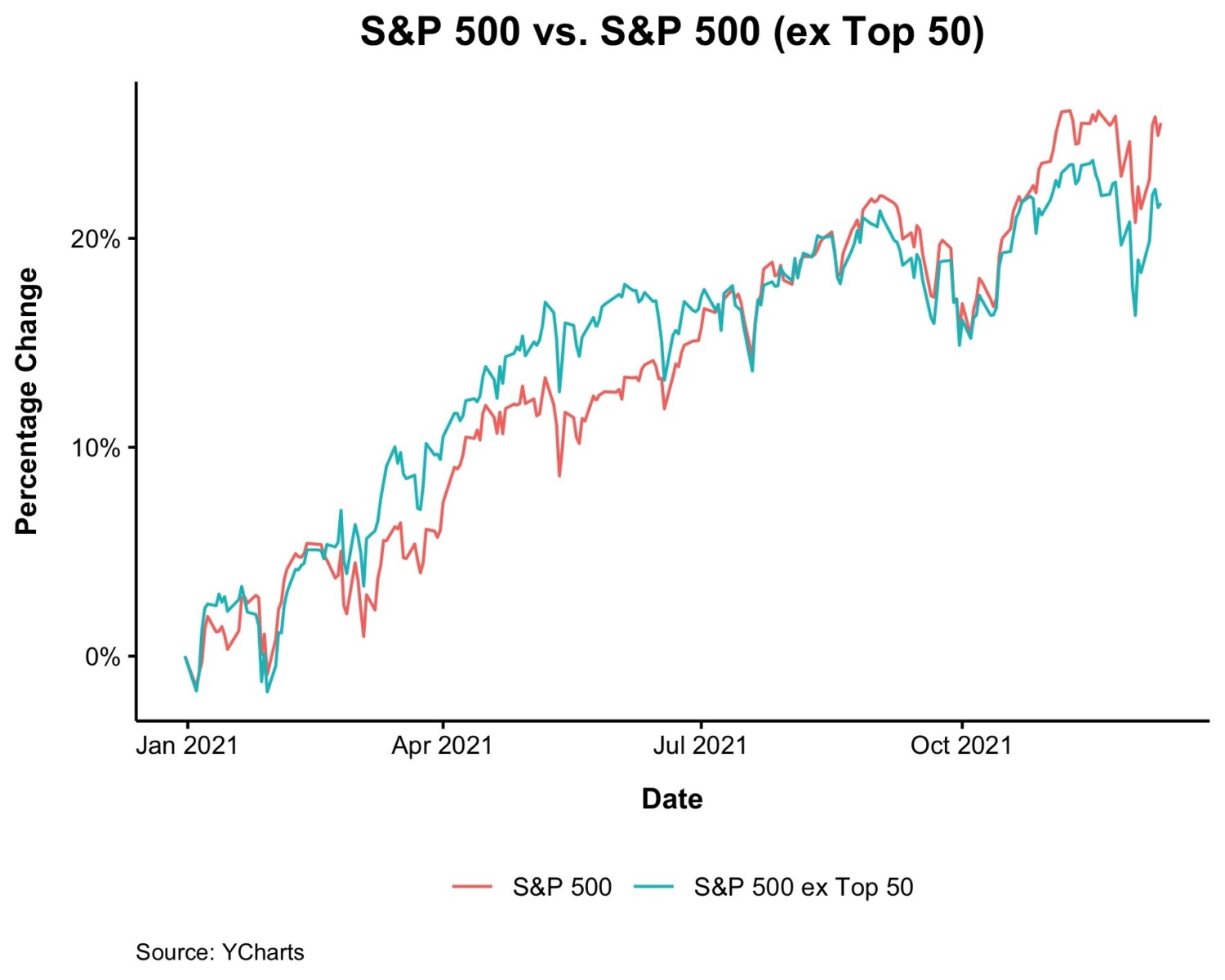

Surprisingly, the top 50 still look similar:

Top 50

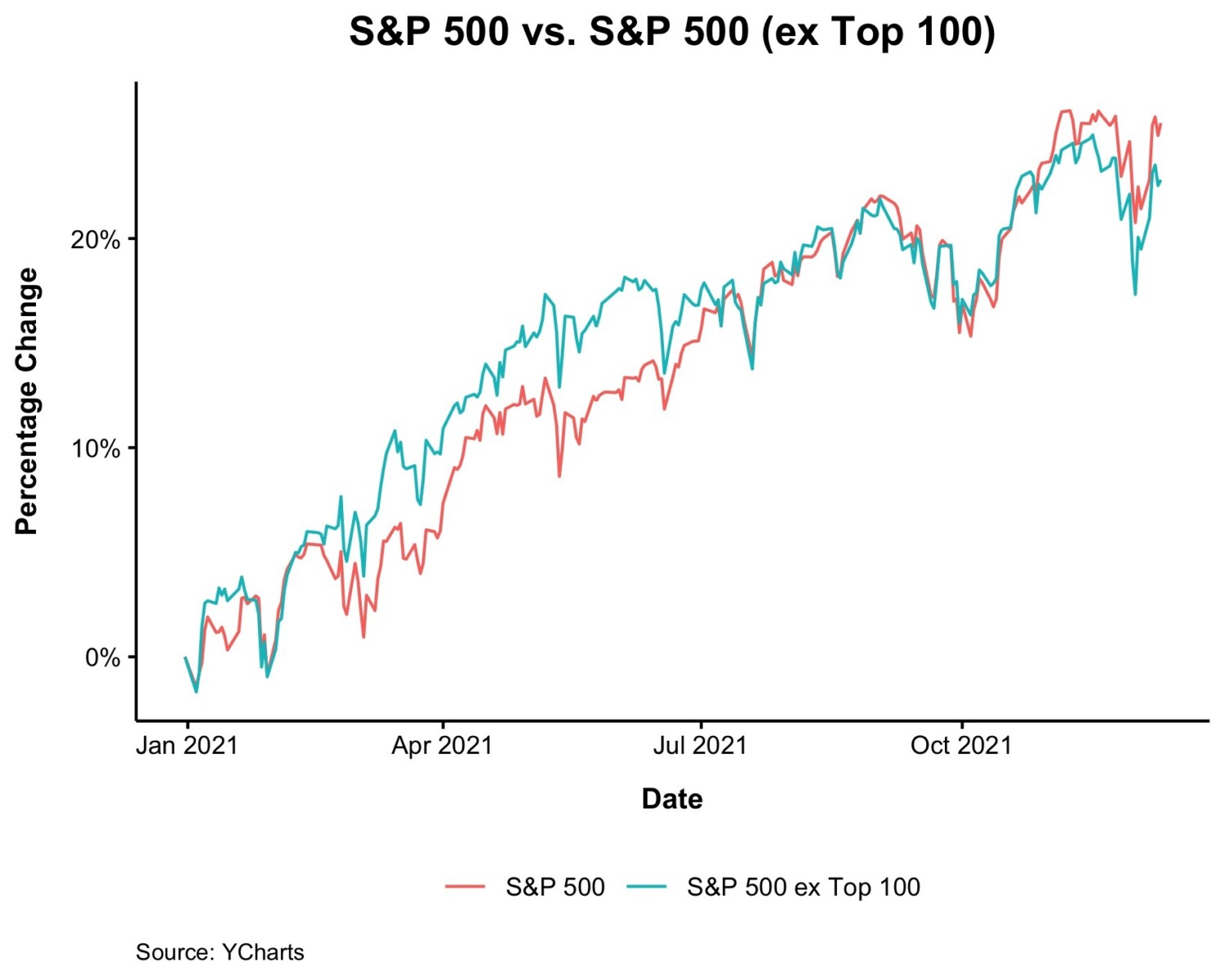

Until we saw SPX 100 and the next 400 names, the advantage of large-cap technology stocks disappeared. The performance of these two groups is very similar in nature—they are both large exponents.

Top 100

The largest stocks account for the majority of market earnings. This is both quite typical and a causal problem: most of the biggest winners have a reason. (I will discuss this next time)

Before:

How to mislead data, big company version (November 12, 2021)

Criticism of concentration index risk is off-basis (August 21, 2020)

So few market winners, so much self-respect (September 26, 2017)

Analysis: Most stocks are not good investments. (September 25, 2017)

Are there too few stocks driving the S&P 500 index? (June 20, 2017)

[ad_2]

Source link