[ad_1]

Fearing that many economies will not be able to recover from the pandemic next year, foreign investment in stocks and bonds in emerging markets outside of China suddenly stopped. Omi Kron Coronavirus variants and expectations of a US interest rate hike.

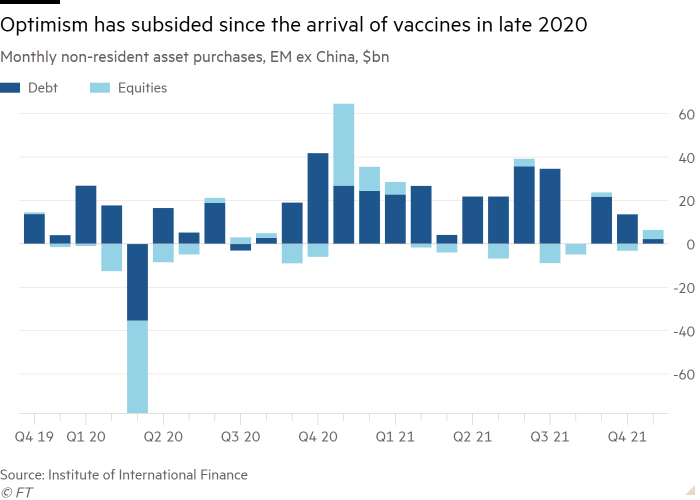

According to data from the Institute of International Finance, in late November, since the market turmoil triggered by the coronavirus in March 2020, non-residents’ capital inflows into emerging market assets other than China became negative for the first time.

“We have seen the willingness of investors to participate in emerging markets dried up,” said Robin Brooks, IIF chief economist.

“This is not just about isolated cases like Turkey,” Currency has collapsed He added that despite the sharp rise in inflation, the central bank has persisted in cutting interest rates in recent weeks. “Turkey is a symptom of the broader foundation of emerging markets, which is the lack of growth.”

IIF separates China from other emerging market data because China’s inflows are so large that it obscures any other trends that may be apparent in the numbers.

According to reports, the emergence of Omicron coronavirus variants in recent weeks will have a greater impact on countries with low vaccination rates. Most emerging market countries have vaccination rates below 70-80% of herd immunity. S&P Research.

Many emerging economies, especially large middle-income countries such as Brazil, South Africa, and India, have also borrowed heavily in the international and domestic markets in response to the pandemic.

Luiz Peixoto, an emerging market economist at BNP Paribas, said that for most of the past year, concerns about the fiscal impact of rising debt “have been unresolved, as if a 10% increase in the debt ratio is meaningless.”

But he said that weak growth prospects means that such concerns are now back. “It doesn’t matter whether you are funded by the local market or the foreign market, because we see interest rates rising everywhere,” he said.

Therefore, Peixoto warned that 10 major emerging markets, including Chile, Mexico, Poland and India, are at risk of downgrading their credit ratings.

What worries investors is that Fed Chairman Jay Powell has recently taken a tougher stance in response to rising inflation.Powell’s open attitude Withdrawal speed is faster than expected The Fed’s massive asset purchase program has improved the prospects for a US interest rate hike earlier next year and has exacerbated the sell-off of risky assets.

A stronger US dollar may destabilize the economic stability of countries such as Turkey, which borrow large amounts of US dollars. Countries such as Brazil, South Africa, and India tend to borrow in their own currencies, but mainly rely on foreign capital inflows.

As the U.S. dollar strengthens, the returns of international holders of emerging market stocks and bonds are eroded. MSCI’s emerging market stock index has fallen 4% this year in U.S. dollars, which is far behind the index provider’s 19% gain, which is widely measured by developed market stocks.

Bonds are also under pressure. The JPMorgan Chase Global GBI-EM Index tracks emerging market bonds issued in local currencies, and has fallen 4.5% in terms of total returns and U.S. dollars so far this year.

In the first few months of the coronavirus pandemic, the depreciation of the U.S. dollar boosted emerging market assets. But with the increase in vaccination rates and the US economy starting to recover this summer, the dollar has appreciated.

The Fed has cautiously hinted that it intends to withdraw from stimulus and tightening policies, which means that the market will not repeat the mistakes of the “shrink panic” in 2013, when the sudden change of Fed information led to a sudden sell-off of risky assets, including emerging market stocks and IIF’s Brooks said .

But a combination of weak growth and a strong dollar is still possible Trigger a sell-offHe warned, especially considering the continuing uncertainty of the pandemic and the growing tensions between the United States and China and Russia.

IIF data shows that foreign capital inflows into emerging market stocks and bonds peaked in the fourth quarter of 2020, just before vaccines in advanced economies became widespread. Since then, the recovery of the United States and other developed market economies has damaged emerging market assets.

But the inflow of funds did not stop until this quarter when the Federal Reserve began to tighten monetary policy. The reduction in the Fed’s monthly asset purchases of $120 billion supports the U.S. dollar because it shows that the Fed is closer to raising interest rates, which is an important driver of global currency valuations.

This pressure has only intensified since the so-called Powell turn on November 30, when the chairman of the Federal Reserve stated that he no longer believed that inflationary pressures were temporary and implied that the central bank was willing to accelerate the pace of monetary tightening.

“Powell’s shift has exacerbated already difficult adjustments in many developing countries. Although the relative yields of emerging market local currency bonds are attractive, investors may now face further pressure from interest rate hikes and weak currencies,” T Rowe Price’s investment Said portfolio manager Samy Muaddi.

[ad_2]

Source link