[ad_1]

just plugged in”Portfolio for long-term investors“Again, I really should have my opinion on its message about the recent stock market downturn. If you don’t see this coming and exit early, or if it’s obvious that this is coming but you don’t get to put your ass down, do Anything, rather self-righteous at the dinner table, how bad should you feel about it?

Not as bad as you might think.

This time around, one can make a plausible reason to push the market lower: Investors find that the Fed will eventually raise interest rates to fight inflation. Prices are somewhat sticky, and higher nominal interest rates will mean higher real interest rates, higher real discount factors, and higher expected returns on stocks without a change in the equity risk premium. Therefore, lower prices today are matched with higher returns in the future, just as lower bond prices are matched with higher yields. In this argument, lower prices don’t mean lower earnings or dividends.

If that’s the case, then long-term investors really haven’t suffered any decline in long-term purchasing power. If your plan is to hold the stock for the long term and effectively live off the dividend (including all cash flow), nothing has changed. Of course, it’s better if you get out of the woods and sell before the dip. But efficient market timing is hard to come by as a consistent strategy. Maybe inflation is just a “temporary” “supply shock” and the Fed doesn’t have to do anything.

Again, should you sell now? So, whether the Fed likes it or not, has the market already priced in all the rate hikes that could come from the Fed or the market? Perhaps the Fed was right in predicting that inflation will largely disappear this year. Maybe not. Bet. Also, if you sell, you have to have the courage to jump back when it looks the most bleak. Efficient market timing is difficult as a consistent strategy.

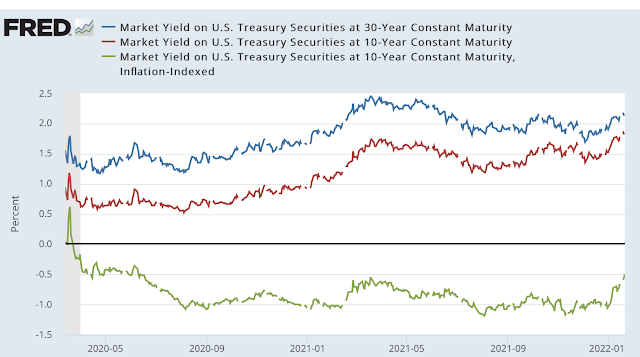

Is this story right? Interest rates are rising, but are they rising enough? Here are three interest rates, 10-year and 30-year Treasury bonds, and 10-year index TIPS. The uptick was noticeable, but it didn’t collapse, and it was still smaller than the uptick earlier in the year. Drag from the back of the envelope, the S&P 500 is down about 10% from its peak. Bond yields rose about 0.5%, meaning the 10-year bond was down about 5% in value and the 30-year bond was down 15% in value. So we’re roughly on the field.

Of course, not everything else is the same. Higher interest rates could reduce those cash flows. Or higher interest rates might fight inflation, thereby increasing real cash flow. Now let’s get back to gambling.

Today’s focus is on realizing a simple possibility: when real interest rates rise, other factors remain constant, and stock prices fall, but (by definition, since I say other factors remain constant) dividends and earnings are not expected to decline. Long-term investors won’t be hurt. The value you get from selling all your stocks has gone down, but so has the cost of rebuilding your portfolio and making a living from it. Likewise, if all the houses have gone down in value, you don’t really care about the first order, because the value of the house you want to buy has dropped as much as the value of the house you want to sell. In fact, you can save on property taxes and capital gains taxes.

[ad_2]

Source link