[ad_1]

Ive here. Larry Summers Warning! He is still among us, and to make matters worse, there may be authorities listening to him. Think of this article as something McKinsey is also touting: leading conventional wisdom. The article uses unemployment data to argue that it shows that the economy is overheating, so it makes perfect sense for the Fed to stomp on arrogant workers to stem inflation, as the Fed has been using recessions to hit workers’ wages. decline. You’ll be surprised to note that it doesn’t mention what people in the real world and what most economists believe are current inflation: supply chain issues, high energy prices, high food prices, commodity shortages. Now, thanks to the backlash against Russian sanctions, those conditions are made worse.

As for the little story about the tight labor market, you can see that the labor force participation rate is still lower than it was when Covid hit:

The reason for the low formal unemployment measures is that people who were previously in the labor market are no longer there. Some people, especially in the medical field, retire early. Some people are chronically infected with Covid and either don’t work or work reduced hours. Some people are no longer willing to go to low-paying workplaces with high Covid risk. It’s not clear how they feed themselves, but the fast food restaurant was among the walking casualties.

By Alex Domash, Fellow, Mossavar-Rahmani Center for Business and Government, Harvard Kennedy School, and Lawrence H. Summers, Professor and President Emeritus, Charles W. Elliott University, Harvard University.Originally Posted in VoxEU

With U.S. inflation reaching 7.9% in February 2022, the Fed raised the federal funds rate by 0.25 percentage points at its March meeting. The latest summary of economic forecasts (2022) released by the Federal Open Market Committee (FOMC) at the same meeting expected interest rates to reach 1.9% by the end of 2022. In response, there has been much discussion about the rationality of the central government. Banks can achieve a soft landing without tipping the U.S. economy into recession.

While designing a soft landing is historically very rare, Federal Reserve Chairman Jerome Powell told lawmakers in early March that he thinks achieving a soft landing is “more impossible” (Powell 2022). This is supported by the FOMC March forecast (FOMC 2022) and the consensus forecast from the Philadelphia Fed’s Survey of Professional Forecasters (FRBP 2022): In both projections, inflation will fall to 3% by 2023 Below, the unemployment rate will remain below 4%.

To test the soundness of the Fed’s forecasts, we looked at quarterly data going back to the 1950s and calculated the likelihood of a recession in the next 12 and 24 months based on proxies for inflation and unemployment. Our analysis is based on the fact that overheating conditions such as low unemployment and high inflation typically lead to recessions in the short term. For example, Fatas (2021) shows that the U.S. economy has never experienced the markedly low and stable unemployment rates predicted by the FOMC.

Our core finding is that, given the current inflation rate of nearly 8% and unemployment below 4%, historical evidence points to a very high probability of a recession in the next 12 to 24 months.

Historical evidence points to a high probability of a recession

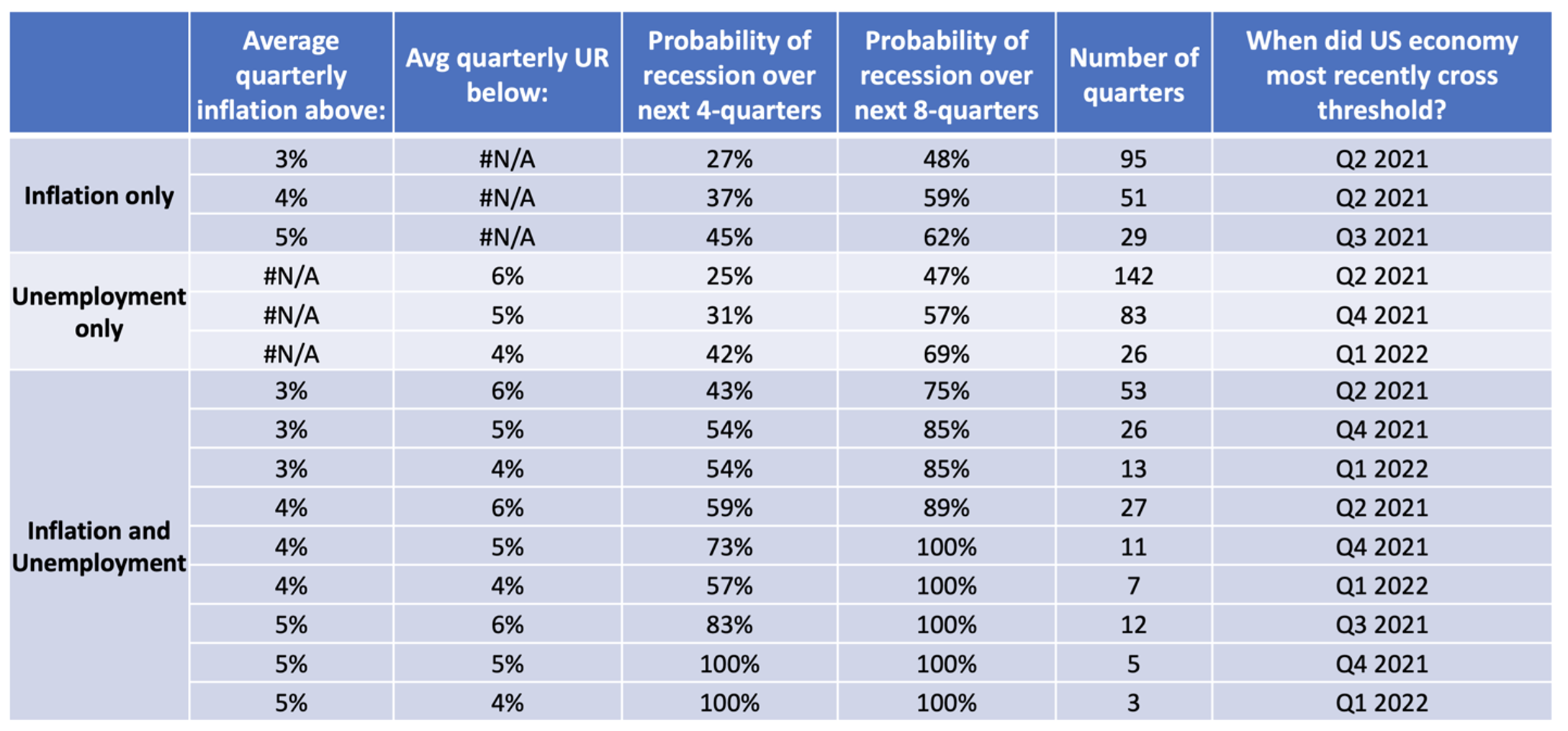

Table 1 shows the historical probability of a recession in the next one and two years, conditioned on measuring both CPI inflation and unemployment. The results show that lower unemployment and higher inflation significantly increase the likelihood of a subsequent recession. Historically, when the average quarterly inflation rate rises above 5%, the probability of a recession in the next two years is above 60%, and when the unemployment rate falls below 4%, the probability of a recession in the next two years is closer to 70% .

Not since 1955 has inflation averaged above 4% in a quarter and unemployment below 5% without a recession in the following two years.

Table 1 Historical probabilities of recessions conditional on different levels of CPI inflation and unemployment, using data from 1955-2019

The results above do not reflect our use of the CPI rather than a proxy for inflation, or the unemployment rate rather than a proxy for labor market tightening. We advocated in our previous work (Domash and Summers 2022) using the job vacancy rate as a measure of labor market tightness, suggesting a higher likelihood of a recession in the next 12 and 24 months. Likewise, using core PCE inflation or wage inflation instead of CPI would lead to the same conclusion.

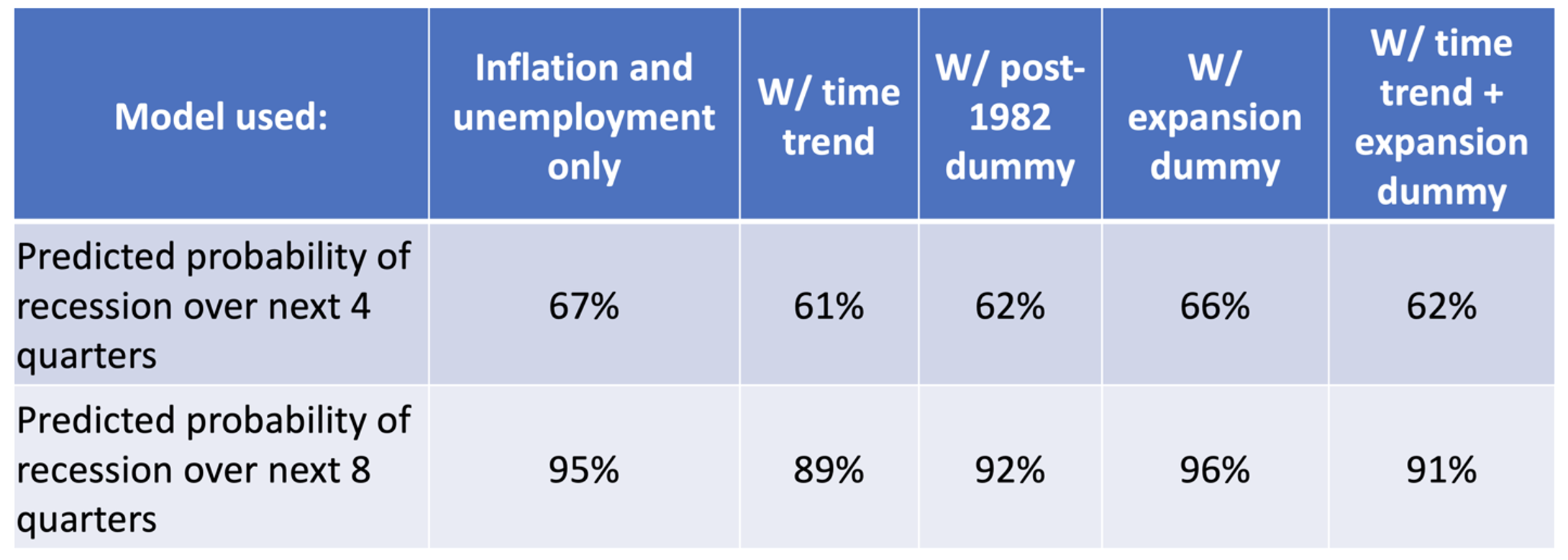

Some might argue that the historical data in these tables overstates the likelihood of a recession because there has been a trend in recent decades for more stable business cycles. Out of this concern, and to maximize the use of available information, we use probabilistic models to predict the probability of future recessions based on current economic conditions and controlling for time trends.

Table 2 presents the results of our probabilistic model, showing the predicted probabilities of a recession in the next 12 and 24 months for five different model specifications. In our baseline model, we use a four-quarter inflation tracking average and a quarter unemployment rate lag as our main explanatory variables. To account for the possibility that recession probabilities have fallen over time, we also develop a specification that includes time trends (column 2) and dummy variables for years after 1982 (column 3). We find in our regressions that trends in business cycle stability do not emerge in any significant way once economic conditions are controlled for. Finally, we include a dummy indicator of whether more than six-quarters of the economy is in an expansion (column 4), as well as time trend and expansion dummy indicators (column 5).

Table 2 Predicted probability of recession in the next 12 and 24 months

These results suggest a very high probability of a recession in the coming years and are robust across many model specifications. Furthermore, the findings do not reflect our choice to use the CPI as an inflation measure or the unemployment rate as a slack measure. Using wage inflation instead of CPI results in a higher forecast of recession probability, while using core PCE inflation results in a similar forecast. Replacing the unemployment rate with the vacancy rate, which we think is a better indicator of austerity, also improves the predicted probability of recession in the next few years.

Overall, we provide evidence that designing a soft landing is very difficult in a rapidly growing inflationary economy.

Soft landing is unprecedented in U.S. history

Some argue that there are reasons for optimism based on multiple soft landings in the postwar period, including 1965, 1984, and 1994. However, we show that some of these periods of inflation and labor market tightening in each country bear little resemblance to the current moment. Table 3 summarizes labor market conditions during these so-called soft landings.

table 3 Labour market conditions today compared to past periods

notes: This table uses quarterly averages for the first quarter of the tightening cycle

In all three events, the Fed operated in an economy with significantly higher unemployment than today, a significantly lower vacancy-to-unemployment ratio than today, and wage inflation still below 4%. In these historical examples, the Fed also raised interest rates well above inflation—unlike today—and explicitly acted ahead of time to stop inflation from rising, rather than waiting for inflation to be too high. These periods also did not involve the major supply shocks that the U.S. is currently experiencing.

With inflation near 8% and unemployment below 4%, the Fed is well behind the curve today and must now catch up to try to contain price increases. America’s historical experience is not a reason for optimism, but a rapidly slowing inflation slowdown always leads to a substantial increase in economic weakness. Our conclusions echo those of Ha et al. (2022), they argue that bringing inflation back to target may require a stronger policy response than currently anticipated. Furthermore, any calculations in this column do not take into account the recent supply shocks associated with the Ukraine war, which only further increases the likelihood of a recession. Therefore, we think the probability of the Fed achieving a soft landing for the economy is low.

As U.S. inflation accelerates, the Federal Reserve will raise interest rates in hopes of a soft landing for the economy. This column uses historical data on unemployment and inflation to assess the likelihood of the Fed reducing inflation without causing a recession. The authors found that both low unemployment and high inflation are strong predictors of future recessions, while today’s overheating indicator suggests a very high probability of recession in the next two years. The odds of the Fed achieving a soft landing for the economy appear low.

Look original post for reference

[ad_2]

Source link