[ad_1]

Just this weekend, Turkish President Recep Tayyip Erdogan reiterated his unorthodox views. theory Lower interest rates will create a “new economic model” for his country.

President Say The interest rate cut will reduce inflation and increase investment, employment and exports, and strengthen Turkey’s independence from other countries.

However, his economic experiment of lowering interest rates instead of raising them in the face of inflation has plunged his country into crisis, currency collapses, soaring prices, and companies struggling with input costs and deep troubles, especially the poorest.

This shows that Erdogan’s views are seriously flawed-standard economic theory is also flawed. Standard economic theory suggests that interest rates need to be raised to defend the currency by preventing capital outflows, depressing domestic spending, and that the authorities are serious about seeking to prevent an inflation spiral.

After the lira depreciated by more than half against the U.S. dollar this fall, Turkey’s inflation rate is heading towards 30%-although on Monday after Erdogan announced compensation for bank lira holders in case of further currency depreciation There was a rebound later.

However, the economics community itself also questioned the role of hot money flowing into and out of emerging economies and the traditional theory led by Professor Hélène Rey of the London Business School, who pointed out in 2013 that emerging markets are often driven by capital flows. The policies of the Federal Reserve and other major central banks.

The International Monetary Fund even outlined a model in which higher interest rates may lead to higher inflation.This work documents Olivier Blanchard, the former chief economist of the International Monetary Fund, and his colleagues pointed out that large inflows of capital into emerging economies—usually brought about by high interest rates—may lead to “credit booms and increased output” and inflation.

But even though the International Monetary Fund-the high priest of economic orthodoxy-published such papers, these conditions do not apply to Turkey.

Because imports often exceed exports, the country’s current account has been in deficit, and inflation has remained high: the average annual inflation rate has exceeded 10% in almost all of the past five years. This indicates that there is a potential price increase problem in the system, and the policy has hardly eliminated it.

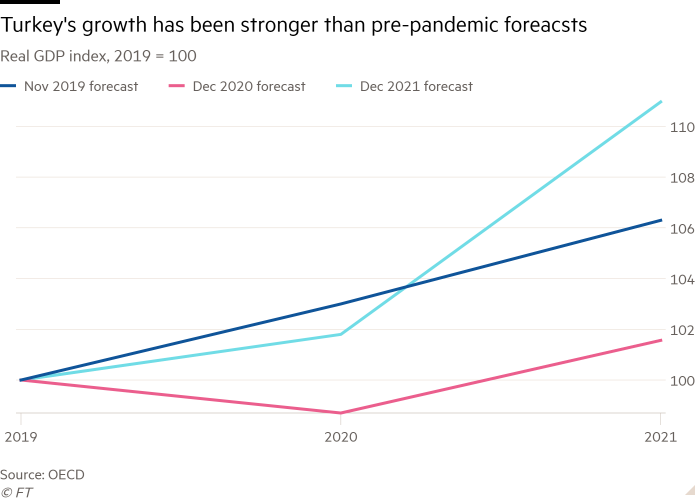

Earlier this month, the OECD stated in Paris that since the beginning of the pandemic, Turkey’s subsidized loans to domestic companies have further pushed up inflationary pressures this year, which will help promote export-oriented “rapid growth.” Make its output in 2021 higher than the OECD had anticipated before the Covid-19 attack.

The OECD also warned that Turkey may “be subject to potential further pressure from wages, import costs and producer prices”.

Professor Danny Rodrik of the Harvard Kennedy School said that for many years, Erdogan has been riding a wave of capital inflows that have been attracted by Turkey’s slightly higher interest rates.

“One of the myths of financial globalization is that it enforces the macro[economic] Discipline,” Roderick said, implying that financial markets will ensure that countries implement reliable and sustainable policies that can attract foreign funds. “In Turkey, the situation is the opposite. Thanks to more resilient financial supplies, Turkey’s economic experiment took much longer than expected. Therefore, the economic cost will be greater. “

Both Roderick and the International Monetary Fund believe that even if higher interest rates help attract capital inflows, thereby increasing spending and domestic inflation, Ankara’s correct response should be to tighten policies to offset this impact and accept growth. Slowly support long-term stability and accurately prevent the crisis of confidence that Turkey has suffered in recent weeks.

Instead, Erdogan did the opposite with the help of a carefully selected person Central bank governorIn a series of expansionary measures, Turkey lowered its short-term policy interest rate from 19% in September to 14% on December 16.

The goal is to gradually reduce the value of the Turkish lira and promote exports by increasing the competitiveness of small manufacturing companies, while also shifting expenditures from imports to domestic goods and services.

Although the current account deficit has turned into a surplus since August, this has caused huge losses to the credibility of Ankara’s economic policies and the livelihoods of the Turkish people.

The official inflation rate in November was as high as 20%, and prices rose by 3.5% in the month alone. Many observers believe that this underestimates the true rate of inflation. Even so, when the impact of the plunge in the Turkish lira appears in import prices, it is expected to rise in December.

To make matters worse, the lira plunge has pushed up corporate and government debt and increased foreign currency borrowing. According to OECD estimates, Turkey’s non-financial corporate debt has increased by 20% of GDP since the beginning of the pandemic, the highest among emerging economies.

Even interest rate cuts can no longer ease the company’s financial situation, because financial markets now require greater compensation for risks. As domestic and foreign investors lost confidence in the lira and sought safe hard currency, Turkish government bond yields rose sharply.

With soaring import prices, the economic situation threatens domestic demand; Tim Ash of BlueBay Asset Management stated that the recent 50% increase in the minimum wage will eliminate the cost advantage of currency devaluation.

“if [Erdogan] Have managed to keep [the line] When there is 10 lire to [US] US dollars, maybe they have a chance, but now that inflation has been ruled out, competitive advantage will disappear, and we are in a depreciating inflation spiral,” Ash said.

[ad_2]

Source link