[ad_1]

This article is a live version of our Unhedged newsletter.register here Send the newsletter directly to your inbox every business day

Welcome back. Some things in the second half of August feel like a Sunday afternoon, and the work week is approaching. At least, American consumers seem to have Sunday depression. There are some thoughts on this, and the persistent strangeness of today’s banking industry.

The market roars past the stagflation graveyard

it is good This Sounds terrible:

The consumer confidence index dropped by 13.5% from July [to August], Fell to a level slightly below the April 2020 low of 71.8. In the past half-century, the sentiment index has only recorded greater declines in six other surveys, all of which are related to the sudden negative changes in the economy: the only time the sentiment index has experienced a greater decline occurred in April 2020. The shutdown period (-19.4%) was at the deepest point (-18.1%) of the Great Recession in October 2008. The loss in early August was widespread in the income, age, and education subgroups and was observed in all regions.

That was Richard Curtin, the economist in charge of the University of Michigan survey. He called the results “shocking.”

The market doesn’t care. On Friday, after the survey was announced, the stock market rose slightly, and the 10-year Treasury bond yield fell slightly.Maybe it’s the hustle and bustle of corporate news-revenue, earnings, and profit margins expand At the fastest rate in more than a decade-making individual consumers’ concerns become irrelevant. Of course, the pleasant background makes the result more likely to be written off, because it reflects two temporary factors: a temporary setback in the fight against the new crown virus, and a temporary spike in prices.

The “This is a complete abnormality” school will not be bothered by this chart, which plots the relationship between the level of consumer sentiment surveys and the year-on-year changes in consumer spending (data from Refinitiv):

In the three periods of the past two decades, marked by the red arrow above, sentiment dropped sharply, followed by a rapid slowdown in spending. The notable exception appears to be the fall in sentiment in mid-2015, which coincides with weak spending, rather than preceding weak spending. Maybe the graph is just noise, but it makes sense to me that people who feel bad about the economy will continue to spend less money.

Strategas economist Don Rissmiller pointed out that the prospect of weak spending, coupled with the still high inflation expectations (around 3%), may indicate stagflation. Stagflation is very bad. However, if we do get it, Rissmiller thinks it might be a mild example:

So far, the spike in consumer prices in the United States has been linked to the “reopening” of industries (cars, hotels, tourism). However, global supply constraints seem to continue to put pressure on prices and expectations. We do not have the 1970s-style stagflation, but we are still uneasy about underlying inflation dynamics (for example, local rents and wages are starting to rise).It’s not easy to ignore a form of stagflation here

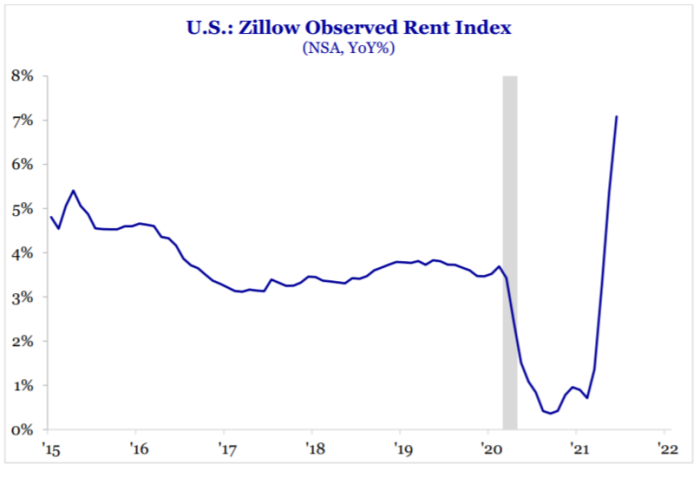

This point about rent is particularly important because rent increases will not be reversed. For example, Ries Miller pointed out that Zillow’s rent index:

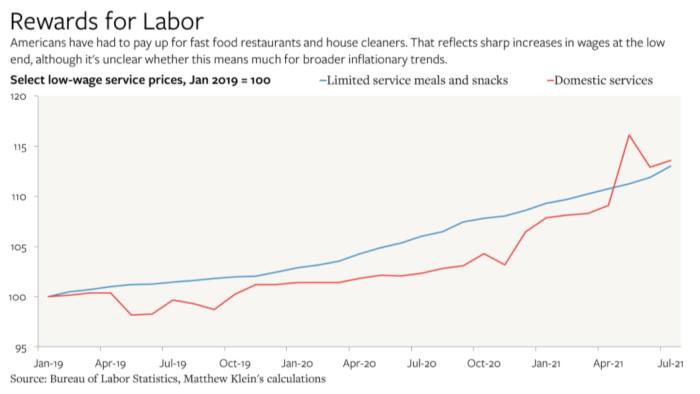

Matt Klein, in Overshoot, Is a persistent and well-informed member of the population where inflation is temporary. But even the wise Klein pointed out that the prices of fast food restaurants and cleaning companies are rising, which may be due to rising wages. He believes that the trend is worth paying attention to:

When the workers with the fewest get more, we are all happy. But what this means for the economy is unclear.

Over the years, almost everyone has systematically overestimated their inflation forecast, which should make us humbly predict that it will increase now. Most of the inflation we see is temporary, for many good reasons, and many measures seem to have peaked. But in general, given that some historically sticky prices are rising and the money supply is growing so fast, continuing to rise rather than crazy inflation seems to be a possibility. Coupled with lower spending, higher inflation will be hurt. The reinflation transaction may be dead. The problem of inflation/stagflation still exists.

Banks: The Worst Cartel in the World (Part One)

This is William Cohan, writing In FT last week:

Overturning the established bank franchise has become extremely difficult. The barriers to entry into the global banking industry have become so great—between strict regulation, huge capital requirements, huge balance sheets, and customer loyalty—they have become cartel-style fortresses.

I think Cohan has a problem here, but his core observation is completely correct. In theory, the business of a bank is prudence and customer service. They are stewards of capital and risk managers; because they mainly sell commodities, relationships and stability are the key. But they often fall into chaos and laugh at these values-which does not seem to cause them much lasting damage, as long as they manage to remain solvency. This is strange.

Think of Credit Suisse. Recent events (Spygate chaos, Greensill chaos, Archegos chaos) have proven the incompetence of serials and comedies. However:

No one expects Credit Suisse to follow the path of Lehman Brothers. Although the damage to the reputation of the big banks makes news reports fascinating, it is also fleeting. Has JPMorgan Chase suffered the lasting impact of the London whale trading scandal? Did Goldman Sachs still miss a beat after the global criminal reconciliation of its role in the looting of Malaysia’s national fund 1MDB? Did Morgan Stanley lose $1 billion because of its Archegos, or was it lost $9 billion by traders in 2007? of course not. These companies are stronger than ever and harder to penetrate.

Cohan didn’t even mention Wells Fargo, which opened thousands of fake accounts to achieve stupid performance goals, and then explored its response to the scandal. Wells’ stock has plummeted, and the cost of rebuilding its compliance and control system is high. But in terms of loans and deposits, it is still the third largest bank in the United States, because prudence and ability do not seem to be important for the basic business of a large bank.

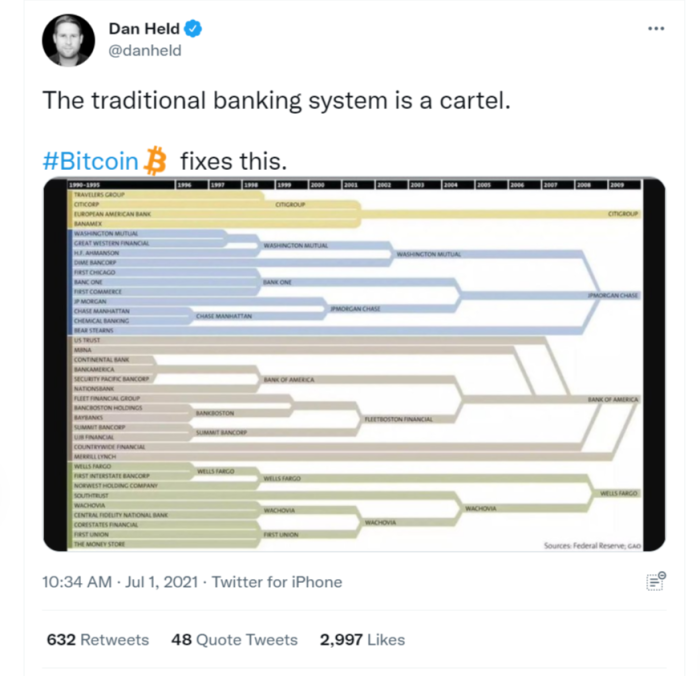

Cohan explained the mystery by saying that the banking industry is a cartel, in other words, an association that hinders competition. This is a popular enough idea, especially among Bitcoin Brothers:

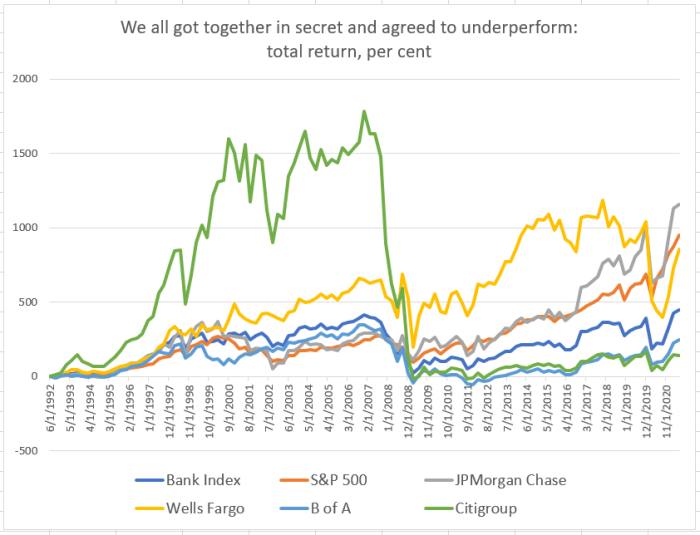

However, this is how it is. If bankers form a cartel, they will hate the cartel. For example, here are the long-term returns of the KBW Bank Index, the S&P 500 Index, and the four large integrated banks in the above tweets:

For the past 30 years or so, this has been the result of the conspiracy of the evil banking conspiracy: only one of the Big Four banks (JP Morgan Chase) outperformed the S&P 500 Index. The fourth largest bank (Citigroup) has achieved a few miserable percentage points in a year of return. The U.S. banking industry as a whole achieved half of the index’s return.

I should point out that the return on equity of banks has been pretty good in the past year or so, because the government has basically assumed all the credit risks and the capital market has gone crazy. But this will end, and at some point, even the return on equity of large banks will fall back to a few percentage points of their cost of capital.

The natural and convincing response to this simple point is that the cartel is not for the benefit of shareholders, but for the benefit of bank executives. Spend several years among the executives of a large bank, no matter how incompetent, your grandchildren will never have to work a day.

Therefore, the return on equity of banks before executive compensation may be better. But the cartel label is still not suitable. For example, banks seem to have very little pricing power in retail, commercial banking, and transaction services. In areas where they do have pricing power (IPO and M&A fees, overdraft fees), in addition to cartel-like entry barriers, other interpretations also apply.

So a mystery remains: if banks are not cartels, why are they so resilient in the face of their own failures? Talk about this tomorrow.

A good book

This An article written by my colleagues Robin Wigglesworth and Laurence Fletcher describes the tentative recovery of the hedge fund industry. This reminds me of the old double problem of investment. It is difficult enough to generate alpha by choosing the right asset; choosing asset selectors is equally difficult, or even more difficult. However, one thing is improving. Across the industry, hedge fund performance and management fees are declining.

[ad_2]

Source link